A few years ago an interesting paper called Market Intraday Momentum was published which revealed a simple trading edge for the S&P 500 ETF.

According to the paper, the first half-hour in the S&P 500 predicts the last half-hour. So if the first half-hour is positive, the last half-hour also tends to be positive.

In the rest of this article, we will put this hypothesis to the test and see if there is any edge.

Source Paper

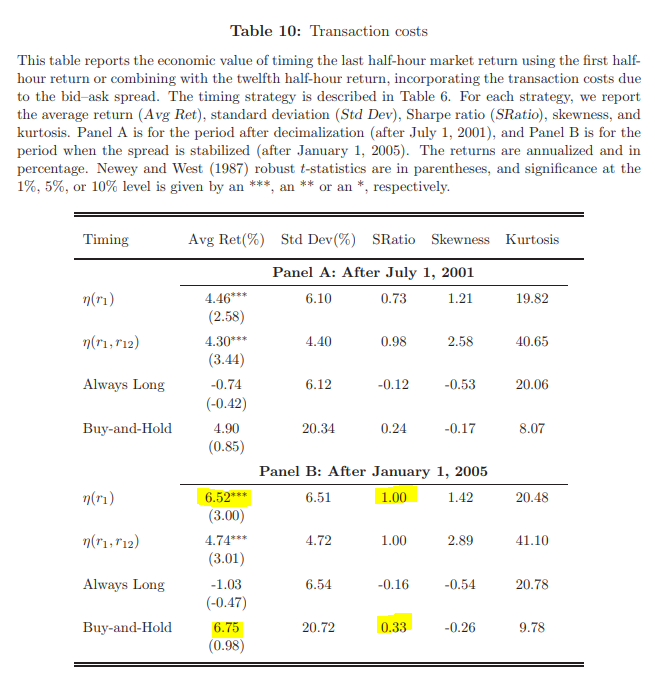

A simple strategy of going long the last half-hour if the market return is positive in the first half-hour was found to produce an annual return of 6.52% (post 2005), with a significantly higher Sharpe ratio (1.0) than buy and hold (0.33).

Furthermore, the authors found that the edge was even stronger during high volume days, recession days and high volatility days. They also found that the edge held up across 10 other ETFs too; QQQ, XLF, IWM, DIA, EEM, FXI, EFA, VWO, IYR, TLT.

It’s important to note that the first half-hour return is deemed positive if it is higher than the previous day close, not the same day open.

Now we know the background to this academic paper we can get to work and see if the results match our own intraday analysis.

1. Test Results For SPY

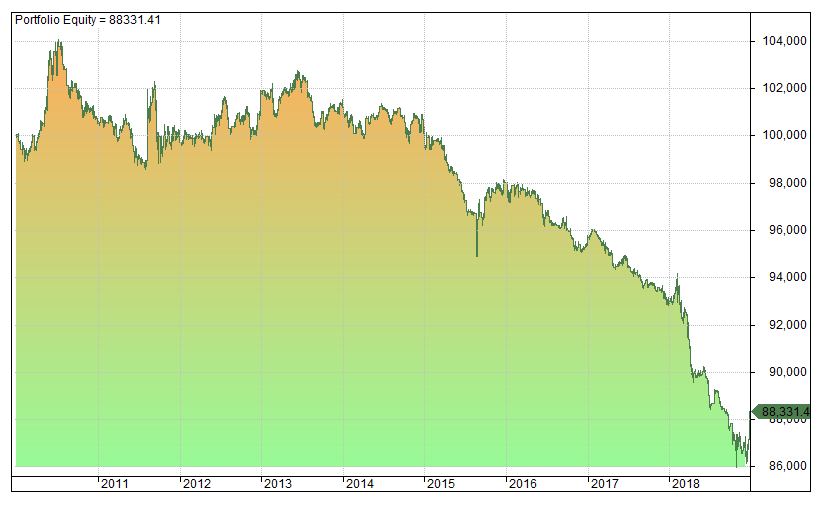

To test this strategy I obtained 5-minute intraday data from eSignal and backtested the following rule on SPY between 1/1/2010 – 12/31/2018:

- If price at 10:00am is > than the previous day close, buy at 3:30pm.

- Sell on the close at 4:00pm.

The following results and equity curve were produced using a full position size of $100,000 per trade with transaction costs of $0.01 per share:

- Net Profit: -11668.59

- Annual Return: -1.37%

- Win Rate: 49.70%

- Average P/L Per Trade: -0.01%

- Sharpe: -2.70

- # Trades: 1165

As you can see, results are not good. We get a negative net profit of -$11,668.59 and an unattractive equity curve.

2. High Volume Days Test

As mentioned in the paper, the strategy works well on high volume days. To test this, we sorted the days into four quartiles based on all 30 minute opening volumes for the past year.

Therefore, we are now trading the same strategy but only on the highest volume days for the past year (i.e. the top quartile):

- Net Profit: -5437.51

- Annual Return: -0.62

- Win Rate: 47.68%

- Average P/L Per Trade: -0.01%

- Sharpe: -5.77

- # Trades: 409

As you can see, we have produced another negative result. Although our net profit is better, our win rate and Sharpe are worse.

3. High Volatility Days Test

We also sorted the days into four quartiles based on volatility which was calculated using % ATR for all 30 minute opens for the past year.

The following results show what happens when we trade the same strategy as 1 but only on the highest volatility days (i.e the top quartile of volatile days):

- Net Profit: -4862.97

- Annual Return: -0.55

- Win Rate: 49.49%

- Average P/L Per Trade: -0.01%

- Sharpe: -5.5

- # Trades: 3

- 90

Once again we have achieved a poor result here and are still not profitable.

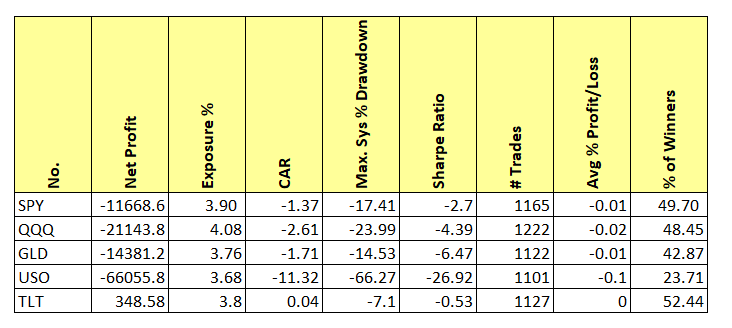

4. Results For 5 Large ETFs

The paper also claimed that the strategy was profitable on a broad selection of 10 different ETFs. However, we tested five large ETFs and once again we found something quite different:

Where Is The Edge?

So far we have tested the momentum strategy from the paper but the results we have produced have been poor across the board.

Perhaps we have made a mistake or perhaps the strategy doesn’t work anymore.

One factor that works against us is the impact of commissions and the very short holding period.

Thirty minutes is simply not enough time in my opinion to capture a meaningful move in SPY, especially in the low volatility environment of the past few years.

Transaction costs of $0.01 per share may also be too restrictive for this strategy and not consistent with what was used in the paper.

However, even if we drop commissions completely, the edge is so minimal there needs to be much more improvement before trading this system live.

Let’s Increase The Holding Time

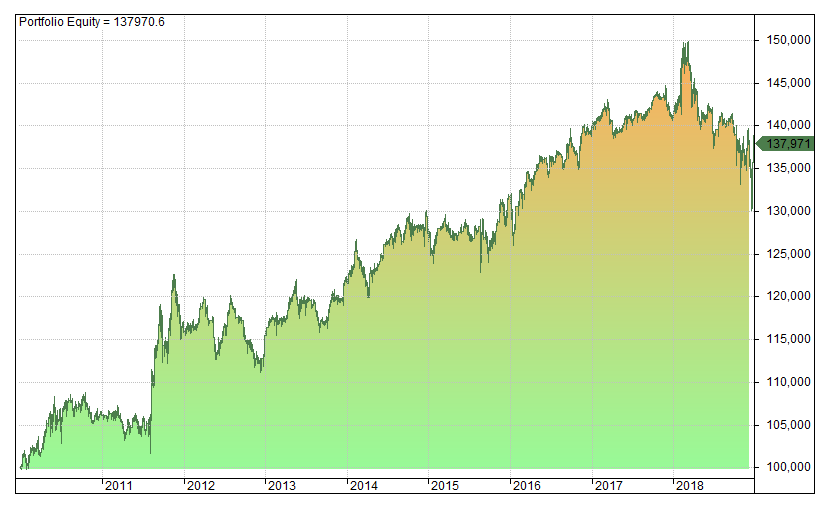

As it turns out, if we increase the holding time we get a much better result than what we have seen so far. This makes sense to me because (as I said already) half an hour is really not long to capture a profitable move.

The following results and equity curve, therefore, show the same strategy but this time we go long much earlier, at 11 am instead of 4pm. This means we have five hours in the trade instead of half an hour:

- Net Profit: 37970.76

- Annual Return: 3.64%

- Win Rate: 56.17%

- Average P/L Per Trade: 0.03%

- Sharpe: 0.44

- # Trades: 1166

As you can see, increasing the holding time gives us a better net profit, win rate and Sharpe. Win rate is now 56.17% and CAR/MDD was 0.27.

You still wouldn’t want to put your life savings on this strategy but it does show improvement.

It also confirms a pattern that I have always held to be true… if you have a momentum signal the sooner you can act upon that signal the better.

Final Thoughts

Academic papers are great sources of inspiration for system traders but unfortunately they do not always hold up to real life trading.

In this article we have tested a simple edge shown in an academic paper but we have found that there is no profit to be found. There might be a few reasons for this:

- The trading edge used to exist but has now been arbitraged out of the market.

- The trading edge was never there and did not exist after transaction costs.

- Differences in the data (particularly the close price) could account for the differences in the results. For example, the paper is using data from TAQ and we are using eSignal.

- Difference in trade commissions. We are using $0.01 per share which is probably too high, however, we also got a poor result with $0.005 and zero commissions. The paper on the other hand ignores commissions but includes a spread introduced by TAQ.

- We have made a mistake somewhere and the results are not representative of the strategy in the paper.

Overall, it is quite surprising that our results are not more in line with those shown in the paper. However, it also seems unlikely that such a simple intraday trading system would work for these ETFs especially in the type of markets we have seen over the last few years.

When you extend the holding time and trade closer to the original signal the results do seem to improve. Much more work is needed before attempting to trade the strategy that is shown in this particular paper.

Simulations in this article produced with Amibroker using data from eSignal.

Hi,

I like your articles. Appreciate the hard work that you put into the research.

Thank you.

Thanks for your comment, cheers.

Really good analysis. I did the same backtest a couple months back and was surprised I got nowhere near the result of the paper. Feels good to have things independently confirmed

Glad to hear you got a similar result, thanks for your comment.

Nice work as always, Joe!

Thanks Kevin!

Hi Joe! thanks for the paper! I am interested in investing in this ETFs I have found a ´mechanical´ trading system that appears to be the best around. I´d like your analytical opinion. It´s End of Day type so that is appealing! It´s call ETF Pairs and the subscription service is wealthsignals.com. It´s shows a backtest and has some tech talk that describes it as purely mechanical.. hmmm! what do you think?

hi Joe,

The original finding compared the return of the first half an hour, so why would you compare the performance at 10:00am instead? I know this is “only” half an hour, but could that be the reason why your results differ from the original findings?

1.If price at 10:00am is > than the previous day close, buy at 3:30pm.

keep on the hard work, much appreciated!

Patrick

Sorry I’m missing your logic here. The rule is the same as in the paper since 10am is half an hour into the day. Am I missing something?

But you developed new strategy instead: shorting last half hour! Does it work on future contracts?