If you want to put your money in the stock market it makes sense to first analyse the data to see whether your trading strategy is a good one or not.

In this article I take a look at three technical trading strategies and see how successful they’ve been over the past 10-18 years.

These ideas are not quite complete but may act as the beginning for your future trading strategy.

1. The Overnight Dump Strategy

Last week we saw the unusual occurrence of a market leader dropping over 10% in overnight trading before bouncing back nearly as much in the following trading session.

The stock I am talking about is of course Netflix (NFLX) which released earnings after the market close on July 16.

The company posted slower growth in new subscribers which did not match investors high expectations.

Netflix closed above its 50-day moving average on July 16 at a price of $400.48 but then hit a low of $344 the next morning, a drop of -14%. The stock eventually finished the day at a price of $379 paring most of that loss.

Historical Analysis

Since 2000, there have been 536 times when an S&P 500 stock with sufficient volume has closed above its 50-day moving average and then opened more than 10% lower on the next open.

According to our analysis, If you had gone long all of those times and exited the trade on the close of the same day you would have won 47% of the time for an average profit per trade of 0.43% before commissions.

Following are some of the backtest statistics generated from this analysis and an equity curve to represent the timeline of results:

- # Trades: 536

- Average P/L Per Trade: 0.43%

- RAR: 123.34%

- Win Rate: 47.95%

- Avg. Win: 5.83%

- Avg. Loss: -4.54%

- Profit Factor: 1.21

Overall, you can see this has been a fairly volatile trading strategy over the last 18 years and most traders would find it hard to follow.

Although the trading statistics are reasonable the equity curve reveals that the system has underperformed since 2010. And this is before commissions have been applied.

Buying S&P 500 stocks after a 10% drop overnight (and exiting on the close) needs some work if it is to be a worthwhile trading system

2. Micro Stocks Mean Reversion Stategy

One of the most recent technical trading strategies to be added to our program at Marwood Research is a trend following system for Russell Micro Cap stocks.

Because of this, I have recently been on the lookout for a mean reversion strategy for the same universe that might help complement this existing system.

The trouble with mean reversion on micro cap stocks is that they are not heavily traded and do not see much news flow. This means they can drift for long periods.

A good trading strategy therefore requires some type of catalyst so that we do not simply trade in stocks that are going nowhere.

Although quite basic, this strategy looks for a new low and uses a spike in daily turnover (volume * close) as a potential catalyst for a rapid move higher.

So we are looking for a stock making a new low that suddenly sees a spike in volume on the next bar and then trades off its lows.

The full rules can be described as follows:

Buy:

- Yesterday’s close < lowest close in 50 days

- AND today’s turnover > $250,000

- AND today’s turnover > 2 standard deviations above the 20-day moving average

- AND IBS > 0.2

- AND today’s close is between $0.5 and $20

Sell:

- Highest close in 5 bars

- OR after 10 days

Trade Example

Here you can see an example of the kind of trade setup we are looking for in OVID:

You can see that OVID hits a new 50-day low on the 10th August 2017. This is followed by a spike in volume on the 11th August and an IBS reading of 0.72.

We therefore go long on the next open (green arrow). 7 days later we hit a new 5-day high so we exit on the next open (red arrow) and we capture a 32.53% profit before fees.

Trade Results:

Plugging these rules into Amibroker and running the strategy on all Russell Microcap stocks between 8/2008 – 1/2018 we get the following results:

(Note that these results include transaction costs of 0.1% per side, fixed position size of $250 and all entries/exits are executed at the next market open. Also note that the data does not go further back than 2008.)

- # Trades: 6052

- Average P/L Per Trade: 1.02%

- Average Bars Held: 6.04

- Risk Adjusted Return: 51.13%

- Win Rate: 53.72%

- Avg. Win: 7.35%

- Avg. Loss: -6.33%

- Profit Factor: 1.35

You can see that these rules have achieved good results across a very large sample of trades in the micro cap space and we have a smooth equity curve.

The results look promising so the next step will be to turn this into a full fledged system with a realistic portfolio size, ranking method and position sizing.

3. Simple Pullback For Futures

The last technical trading strategy I will look at today is the same as I wrote about last week for SPY which is intended to buy short term pullbacks within the long term trend.

I had a number of readers comment about the effective use of capital with this strategy. SPY is not very volatile so we need to tie up a lot of capital trading it.

Therefore, I thought it would be interesting to see how the system fares when applied to some futures markets which offer greater leverage.

In case you missed it, the very simple rules of this system are as follows:

Buy:

- Close > 200-day MA

- AND Close < 10-day MA

Sell:

- Close > 10-day MA

- OR 10% stop loss

Trade Results

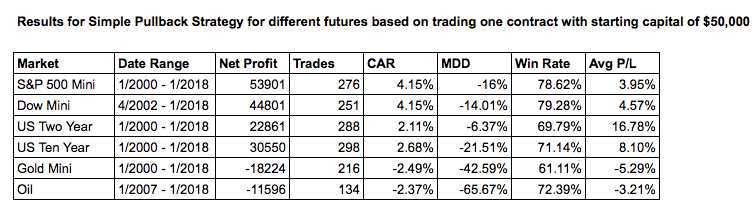

Plugging these rules into Amibroker and running some analysis we can see some statistics for the following futures markets:

As you can see, we have seen robust results across our equity futures (S&P 500 E-Mini and Dow Jones E-Mini). Good results also in Treasuries but poor performance in gold and oil.

These results are based on trading just one contract and before any money management system has been applied. Commissions are set at $10 per side.

As you would expect, the results show this strategy works best during bull markets which was the conclusion from the original article.

Some underlying opinion on the direction of the market or market regime filter is therefore recommended to be used with this approach.

I still feel this can be a good strategy for taking chunks out of a bull market. Using walk forward analysis and adding a short side could be the next step.

Update – Add Short Side To Pullbacks Strategy

After writing this article I decided I would run another simulation for the pullbacks strategy above this time adding a short side and testing on ES (S&P 500 E-Mini). So now we are using the same long rule with the additional short rule below:

(Basically this is the reverse of the long rule, so we are now looking to buy dips in a bull market and short rallies in a bear market):

Short:

- Close < 200-day MA

- AND Close > 10-day MA

Cover:

- Close < 10-day MA

- OR 10% stop loss

Trade Results For ES

- # Trades: 323

- Net Profit: $77,445

- CAR: 5.34%

- MDD: -16.45%

- Avg P/L: 3.66%

- Profit Factor: 1.49

Pleasingly you can see that adding a short side to the ES strategy has improved our trade results.

Our net profit has improved from $53,901 to $77,445 over the same time period while our max drawdown has stayed at a similar level. The equity curve looks reasonably good too.

Obviously, there is more testing to be done with this system and we need to look closer at the stop but the initial results for such a simple system are encouraging.

Charts and analysis in this article produced in Amibroker using historical data from Norgate Data.

Hey Joe,

another great post, thanks for sharing your ideas! I really like the second system, there is one rule I don’t understand: “AND IBS > 0.2”, what IBS stands for?

Yes it’s Internal Bar Strength. It measures the position of the close in relation to the day’s trading range. IBS = (Close – Low) / (High – Low). Zero means the close was also the low and 1 means the close was also the high.