Designing a trading system is about following the right processes and being conservative in your assumptions. I have already talked about the pitfalls of selection bias and I’ve spoken of the importance of stress-testing a trading system thoroughly. Now I shall answer the question ‘what is slippage’ and how does slippage affect trading system performance.

What is slippage in forex and stocks?

Slippage occurs when you place a trade in the market but get a different entry price to what you were expecting. The effects of slippage can therefore be negative or positive for a portfolio – although it’s usually negative.

Negative slippage can be a frequent occurrence depending on the type of market you trade and the type of order you use.

Market orders

If you use market orders or stop orders you are at risk of slippage, since these orders attempt to enter the market at the ‘best available price’.

To understand this, imagine that Apple is trading with a bid/ask spread of 100.4/100.5 and you want to buy. If you place a market order to buy 100 shares of stock, you are effectively saying…

“I don’t care what price I get filled, just give me my 100 shares at any price”.

Let’s say that there are only 10 shares available at the price of 100.5 and the next available shares are at $102. In this instance, your order of 100 shares will be partly filled at 100.5 and the rest will be filled at the next available price of $102!

In other words, you will have paid way too much for your shares and will be staring at a decent sized loss right off the bat.

And it’s exactly the same with currencies. If you place a market order to buy EURUSD, you will get filled at the best price that is available.

Liquid markets

Now of course, in highly liquid markets like Apple, EURUSD or the S&P 500 future, placing a market order like this will not usually end up costing you too much at all. In these markets, there are usually hundreds of bids lined up on both sides, so placing a market order is not necessarily so bad if you want to get in quickly.

The one exception is if there is a big news release coming up or if you are trading during after hours. When a news release comes out, traders sometimes scramble to close and open positions and spreads widen. This means if you place a market order you might not get filled at the price you want. The same goes for after hours, where volume tails off.

Likewise, smaller stocks, exotic currencies, and penny stocks have much less liquidity and for these markets, market orders frequently get filled at a worse than expected price.

Easy solution

Slippage can be extremely expensive but there is a one solution that is remarkably simple and easy: Don’t use market orders!

Instead of using market orders, you can use limit orders. That way, you will only ever get your order filled at the price you specify. By doing so, you may sometimes have to wait a little bit longer to get filled but it’s better than getting filled at a much higher price.

A good rule of thumb is to place an order that is between the bid and the ask.

If you absolutely have to use market orders, it’s a good idea to only trade highly liquid markets. If you have direct market access (DMA) you can also have a look at the order book to see whether there are enough bids to take your order easily.

Taking care of slippage in trading system design

Because slippage can have a negative affect on trading performance it’s necessary to incorporate it into designing a trading system.

When you look at a historical price chart, the prices you see are not the same as the prices that you might have traded. Most charts will show the last price traded, which is not the same as showing the last bid or last ask price.

In other words, you cannot be sure that your order would have been filled at the same price as represented on the chart. For some longer term systems, a bit of slippage may not have a huge effect. And some breakout systems are set up to enter trades on the market open (using market orders).

However, slippage can have a huge impact on short term systems or systems that trade less liquid markets.

The upshot of all this is you need to be conservative when designing your trading system and take some element of slippage into account.

But how?

Simple solution

One way of taking into account slippage when designing a trading system is to simply direct the system to trade on the ‘worst’ available price, instead of the best price.

For example, let’s say you have a system that enters orders on the next day open. Instead of telling the system to buy on the next day open, you tell it to buy on the next day high. Instead of telling the system to sell on the next bar close, you tell it to sell on the next bar low.

By doing so, you guarantee a realistic price fill and make sure to account for the worst effects of slippage.

Alternatively, instead of telling the system to buy on the high and sell on the low, you could specify a half-way price between your intended entry and the worst available price. If you always trade on the open, for example, the Amibroker code is simply:

Buyprice = (O+H)/2;

Sellprice = (O+L)/2;

Thus, your entry is half way between the open and the high. You take slippage into account and make conservative assumptions for what your actual entry price would be.

This is what I do when introducing slippage but if this is too conservative for you, you can try testing various percentage levels, slippage of 1%, up to 50%.

The effect of slippage on trading systems

As I mentioned already, slippage can have a big effect on short-term trading systems and systems that trade in thin markets.

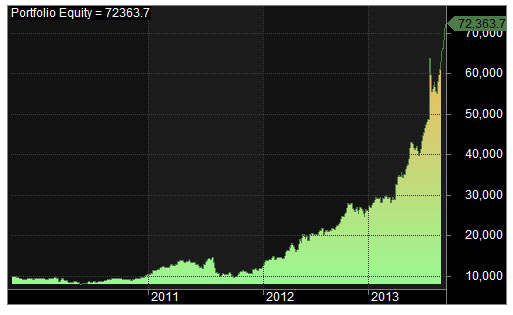

To illustrate the effect of slippage, let’s see what happens when I apply the above process to one of the trading systems from my course: Cherry Picking Penny Stocks with EMA Crossover.

This system uses a simple EMA crossover to find trades and ranks them by size, so that smaller stocks are preferred.

Back-testing this system on the Russell 3000 universe of stocks (delisted stocks not included) between 1/1/2010 and 1/1/2014 gives an impressive return of 64.35% CAR before slippage.

After applying slippage of 50%, the return drops to 57.25% CAR.

![]()

What does this mean?

Well first of all, these results are encouraging. Incorporating 50% slippage, performance does go down but not by much. Since this system trades weekly and is trend following in nature, slippage does not have a huge effect on returns.

Second of all, the returns are quite high, owing to the fact markets have had a stellar couple of years. But this does not mean much until we have run some further tests. The next step will be to stress-test the system further, by testing different start dates and incorporating delisted companies.

Acknowledgements: Trading systems were tested with Amibroker and historical data provided by Premium Data.

Get access to this system and 20 others with my new course and ebook: How to Beat Wall Street