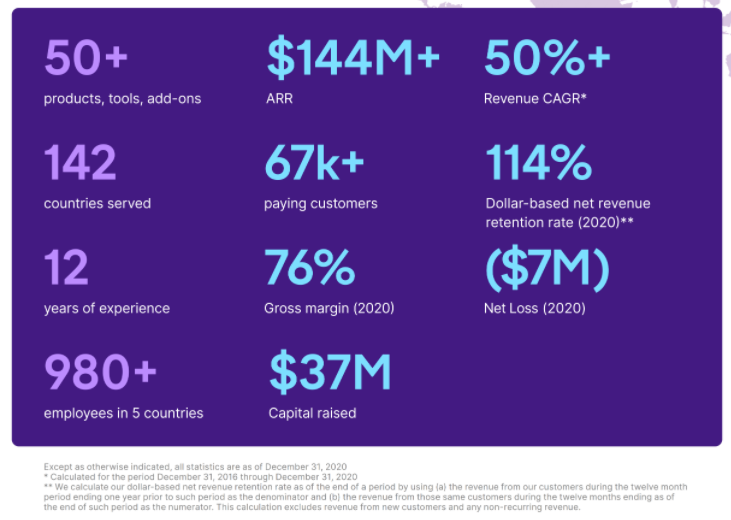

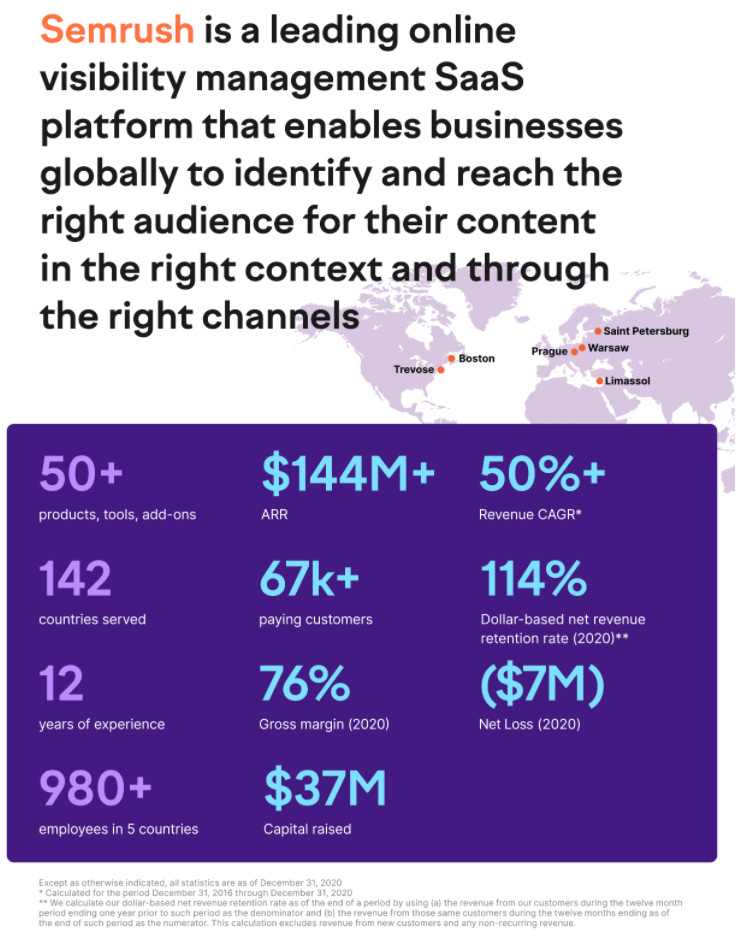

Semrush (SEMR) is a SaaS business directed at online marketers which IPO’d on March 25th 2021. The company boasts annual recurring revenues of $144 million with 76% gross margins and a 50% revenue growth rate measured between December 2016 to December 2020.

The Semrush IPO was not particularly well received as underwriters hoped for a price between $14-$16. However, shares have moved slightly higher since. As of the 6th April, the stock traded at $12.50 a share.

What Does The Company Do?

Semrush provides a SaaS platform that helps companies improve their online marketing efforts. The platform is essentially a ‘one-stop shop’ for search engine marketing with more than 50 tools designed for SEO, online ads, content marketing, social media and market research.

Online marketers use Semrush to perform keyword analysis, schedule social media posts, gain exposure for their websites and spy on competitors. The company relies on a mix of web scraping and third party data to gather insights across 200 million domains, 20 billion keywords and 33 trillion backlinks. This allows online businesses to improve their web presence and action their online strategy.

Case Study

From what I can gather, Semrush is an effective tool and generates a reasonable amount of praise from small businesses trying to compete in crowded markets. The Semrush blog and prospectus contains a number of case studies and success stories. The following comes via a dental practice customer in Liverpool, England:

Smileworks is a dental practice in Liverpool, England that provides dental and medical aesthetics to patients. Before Semrush, Smileworks relied on outbound marketing tools that required considerable investment and did not drive returning clients. Within ten months after starting to use Semrush, Smileworks saw a 4,773% increase in organic traffic to its website. Smileworks was able to obtain the number one position for over 380 keywords locally. In less than five quarters, Smileworks has grown its practice from a margin of (5%) to 38%, with an increase in top line revenue of 100%.

Business Model

Semrush utilises a ‘freemium’ business model. Users sign up for a free trial and are later encouraged to upgrade to a monthly or annual subscription. Prices range from $99 a month for a Pro account to $449 per month for a business account. There are also upfront payment options but over 70% of users pay monthly. As of December 2020 the platform had 404,000 free customers and 67,000 paying customers across 142 countries.

The company also has standalone products in the form of Prowly, Sellerly and Competitive Intelligence which it can use to upsell paying customers and drive more revenue. Prowly was acquired in August 2020. In addition, the company offers a popular affiliate program whereby users of the product can earn up to $200 for referring others to the platform.

TAM

Digital marketing is a growing industry that has accelerated during the pandemic as more and more businesses move online. As the online space becomes more competitive, the tools needed to thrive online face greater demand.

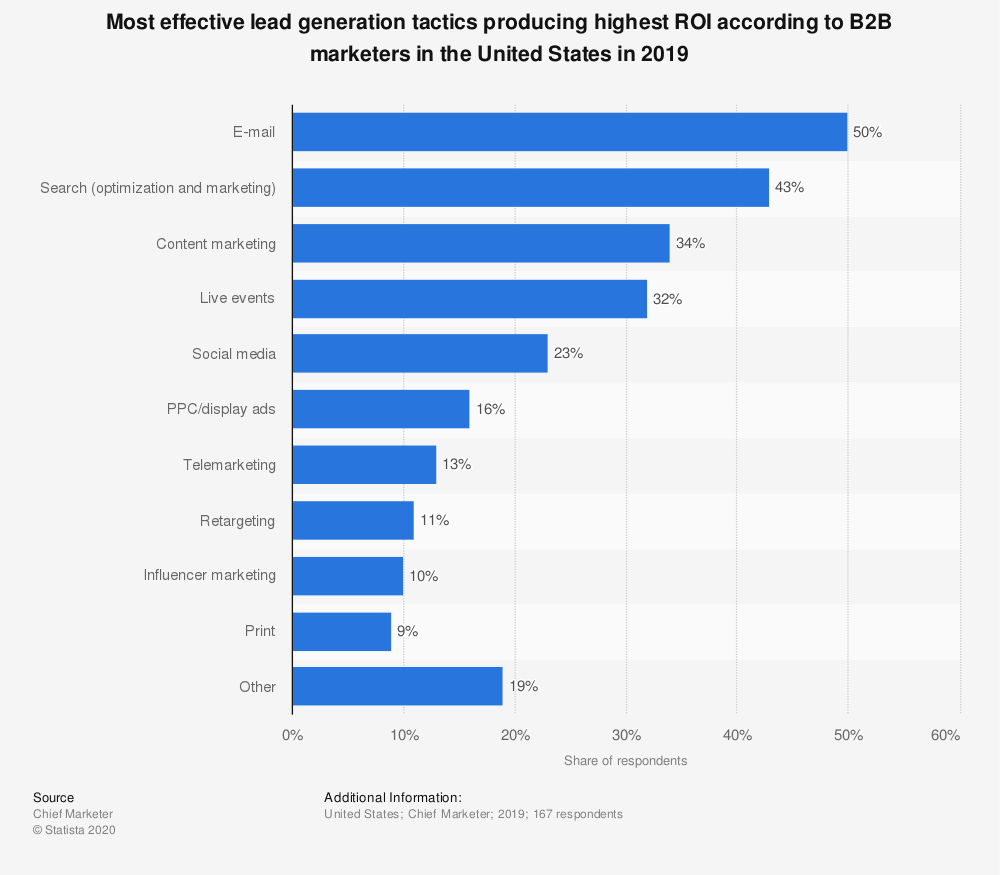

According to Statista, e-mail, search and content marketing were the three most effective lead generation tactics in 2019 ranked by B2B marketers. The continued success of these marketing tactics is good news for a stock like Semrush.

Source: Statista

Meanwhile, a report by Grand View Research estimated the total addressable market for digital marketing software at $43.8 billion in 2019 with a forecast growth of 17.4% CAGR between 2020 – 2027.

In their own prospectus, Semrush emphasised that 94.9% of its customers are small or medium sized businesses with an average annual revenue of $2,000 per user. The company suggests the annual global potential for its SaaS platform is $13 billion (conservative figure). With annual recurring revenues of $144 million, Semrush is therefore operating at a fraction of its potential.

We estimate that, based on our current average customer spending levels, the annual global potential market opportunity for our online visibility management SaaS platform is currently $13 billion.

Competition

The online marketing space is fiercely competitive and this is one of the key risks for investors to consider with Semrush stock. The company’s prospectus underlines this saying

The market for our products is fragmented, rapidly evolving, and highly competitive, with relatively low barriers to entry…Many of our current and future competitors benefit from competitive advantages over us, such as greater name recognition, longer operating histories, more targeted products for specific use cases, larger sales and more established relationships or integrations with third-party data providers, search engines, online retail platforms, and social media networking sites, and more established relationships with customers in the market.

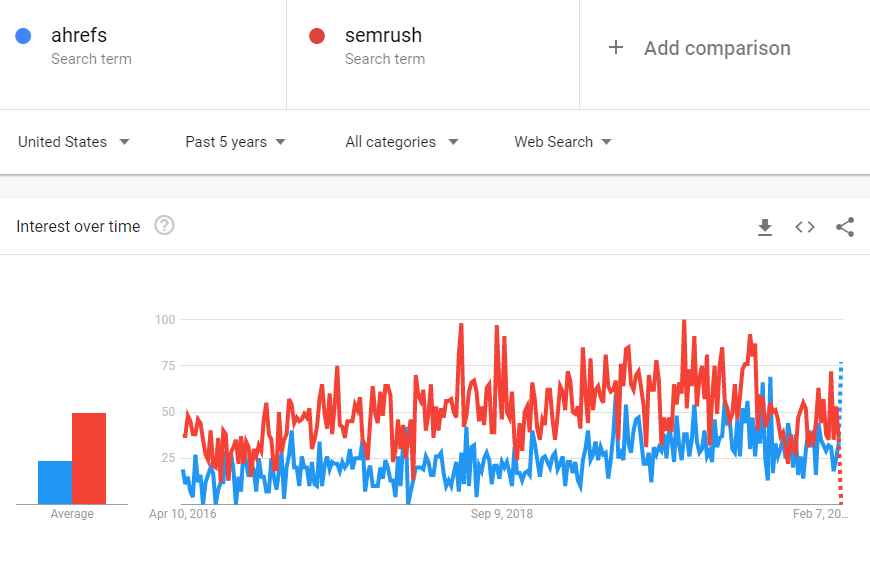

From what I can see, Semrush possesses a relatively strong stranglehold on the SMB market which it shares with another service called Ahrefs. The two platforms offer similar tools and pricing with Semrush seen as the slightly more premium alternative. Both Semrush and Ahrefs garner a decent amount of positive reviews among users in online communities.

Source: Reddit

Semrush also sees a higher share of web traffic according to Google Trends:

Source: Google Trends

As well as Ahrefs there are other competing services that offer similar benefits. Alexa.com, an Amazon company, offers many of the same tools as Semrush and starts at $149/month. Meanwhile, Israeli startup SimilarWeb boasts some large customers and has plans for its own IPO in 2021.

There is also a plethora of smaller companies that offer more tailored, individual services. For example, BuzzSumo is a tool that analyses content ideas and user engagement. HootSuite is a tool specifically for managing social media and scheduling posts and Ubersuggest performs keyword research.

Online marketers therefore have a wealth of choices available to them. They can opt for a platform like Semrush that does it all or they can pick and choose from numerous smaller tools that meet their needs.

On top of all this, Google provides its own free solutions in the form of Google analytics, Google keyword planner and Google search console. You could make the case that Google’s free products threaten paid alternatives since much of the data is controlled by Google itself. However, this is unlikely since Google doesn’t like to reveal too much information about search traffic and keywords. In fact, Google has become increasingly more secretive about its ranking methods which could in fact make tools like Semrush more valuable not less. Google’s products are also harder to navigate and not as intuitive as the paid tools.

From my own trial of Semrush I liked how the platform was organised and I feel it offers valuable insight for online marketers. The software is reasonably priced, has good customer service and a comprehensive knowledge bank supporting the product.

Screenshot taken from a Semrush dashboard.

Management

A plus point for this stock is that the company is led by the two founders Oleg Shchegolev and Dmitri Melnikov who own over 85 million shares between them. Although Semrush began as a bootstrapping project, the founders understand that Semrush now needs capital to invest and continue its rapid growth.

To this end, the company currently pursues several growth strategies:

- Acquire new paying customers and convert the existing base of 400,000 free users to paid.

- Provide upsell opportunities to the existing base of 67,000 paid subscribers.

- Continue to innovate and develop new products and features.

- Pursue opportunistic acquisitions. For example the bolt-on acquisition of Prowly in August 2020.

A Look At The Numbers

As a recent IPO and classified as an emerging growth company that was founded in 2008 the financial history for Semrush does not go back far.

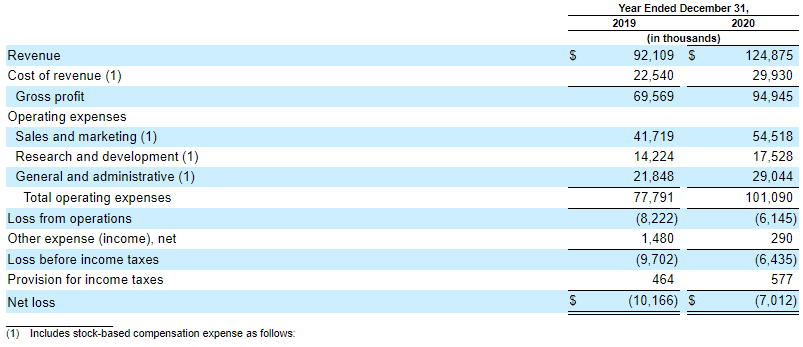

Last year, the company earned $125 million in revenue and spent $54.5 million on sales and marketing. (Note that the prospectus also refers to $144 million in revenue which is an extrapolation based on current subscriber numbers).

Gross profit was $94.9 million while total expenses were $101 million for a net loss of -$7.01 million. Revenues increased by roughly 34% on the year prior, gross profit increased by roughly 36% and cost of revenue increased by roughly 32%.

While it’s good to see revenues increasing, it’s clear that costs of revenue have risen in similar proportions. Sales and marketing is relatively high at around 44% of revenues with R&D only around 14% of revenues.

Source: Company prospectus

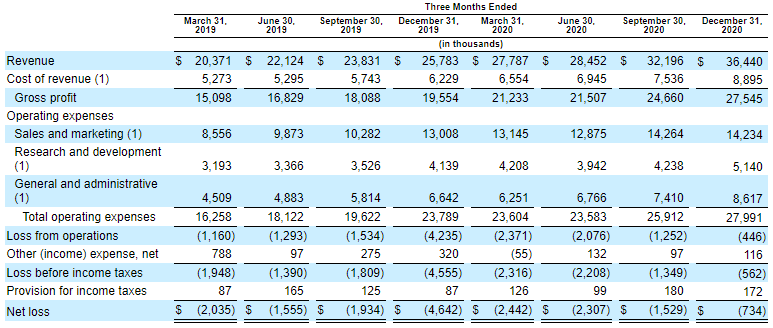

I could not find too many details about revenue in prior years but as shown in the quarterly income statement, revenue has grown in each of the last 8 quarters:

Source: Company prospectus

Looking at user growth, the company had 54,000 paying customers in 2019 and 67,000 in 2020 indicating a gain of 24%. Meanwhile annual recurring revenue per user increased from $1,892 to $2,123. Management maintains that this is one of their key metrics (increasing ARR per user) as it shows an ability to drive long-term value to users.

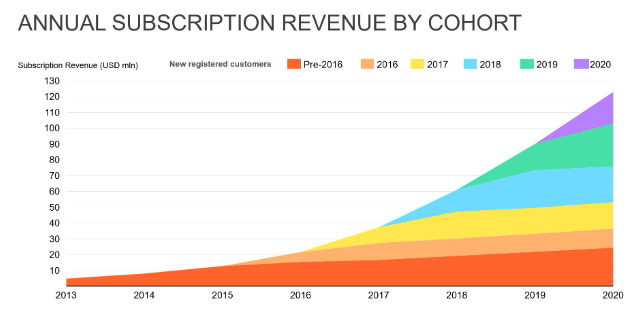

Two promising assertions from the documentation are a 50% revenue CAGR from 2016 – 2020 and a dollar-based revenue retention rate of 114%. The revenue growth speaks for itself. The retention rate means that the average customer on Semrush stays on the platform more than 12 months and increases their spend from the year prior. This is based on 2020 numbers. The following graphic indicates how legacy customers are still heavy contributors to the company’s top line revenue:

Source: Company prospectus

Semrush Stock Valuation

Based on a count of 133.3 million shares and taking into account approximately $160 million in cash raised through the IPO I get a back of the envelope enterprise value around $1.51 billion based on a share price of $12.50. On annual revenues of $125 million that gives us a EV/revenue multiple of just over 12 times which is more or less in line with the median multiple across the sector.

It’s hard to put an intrinsic value on a company that is not yet profitable and is in the relatively early stages of a growth cycle but if we suggest Semrush is able to grow revenues by 20% annually over the next ten years (not unfeasible given the growth potential of the industry and ambitions of the company) Semrush would see revenues of around $770 million by 2031.

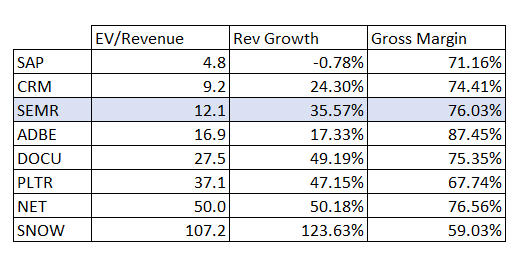

A 10 times revenue multiple on that figure would then put the enterprise value just under $8 billion. Based on the current valuation that would provide an investor today with an 17.8% annualised return. Meanwhile, many SaaS companies are trading at far more extravagant multiples such as those shown below:

It’s worth remembering that while Semrush has the third lowest multiple in this bunch it is also the smallest market cap by some way. It seems to me that Semrush will have plenty of opportunities to continue its growth and meet a required investment threshold.

The recent IPO garnered less attention than I was expecting and that has resulted in a valuation that sits below many peers. The low friction business model and high gross margins means the company shouldn’t have too much problem turning profitable in the near future and the firm is already close to positive earnings per share.

Risks

As I mentioned previously, a key risk with Semrush stock is the competitive landscape. There exists a plethora of products that exist in the same space, some coming from organisations with deeper pockets than Semrush. Apart from mild network effects, I can’t see Semrush as possessing any significant competitive advantages over its peers. That said, Semrush is still a young company and those advantages may come as the business develops.

Another risk is that data providers such as Google may stop third party services from accessing their data. They could introduce features to prevent web scraping which would inhibit Semrush’s platform and make its tools far less powerful for marketers.

Semrush also derives almost all of its revenue from its SaaS platform so there is a lack of revenue diversification if the platform was to encounter decreased demand. Although SEO and SEM are big business right now, there is no telling how the internet might continue to develop and what kind of marketing tools will be needed in the future. See the S-1 for a full breakdown of risk factors.

Final Thoughts

As businesses move online, more of them are learning the benefits of digital marketing techniques like email marketing, SEO and content marketing. As the internet becomes increasingly crowded, businesses look to these tools to help them stand out.

As a result, online marketing techniques are becoming increasingly common and receiving a larger proportion of marketing spend. This leads to a buoyant market for online marketing software and favourable long-term trends.

I think the key point here is that Semrush has proven it has something vauable to offer. The product is a popular choice among small businesses with compounded revenue growth of 50% between 2016 – 2020, strong gross margins and high retention rate.

The company is debt-free and controlled by it’s original founders who are ambitious and have personal stakes in the company. The recent IPO gives the firm capital with which to develop new products and drive future growth.

The space that Semrush operates in is wide but also super competitive and Semrush offers no monopoly over its peers. However, Semrush has proven it has what it takes to occupy a space in the industry and grow revenues at a quick pace.

Strong tailwinds and a well-placed product means Semrush stock is good value at 12 times recent sales. I bought a medium sized position (medium conviction) at a price of $11.51. I plan to follow the company to make sure growth continues at a satisfactory level.

You were right. Thank you.

You’re welcome!