Members of our research program at Marwood Research will know that I update the program with new trading strategies on a regular basis.

Last month was Vix Trio and this month I have included another new trading system (with source code) called VWAP Pilot.

What Is VWAP Pilot?

VWAP Pilot is a simple intraday system designed for US equities that closely follows trends on the 30-minute chart.

The system is similar to the VWAP strategy I wrote about a couple of weeks ago. However, VWAP Pilot is specifically designed to avoid WHIPSAW trades and shows much stronger performance.

Whipsaw trades can be a big problem when using VWAP (volume weighted average price) because price tends to fluctuate above and below this line regularly.

Following you will find some key statistics and charts for the VWAP Pilot system as backtested in Amibroker.

Key Statistics & Charts

Example Trade Setup

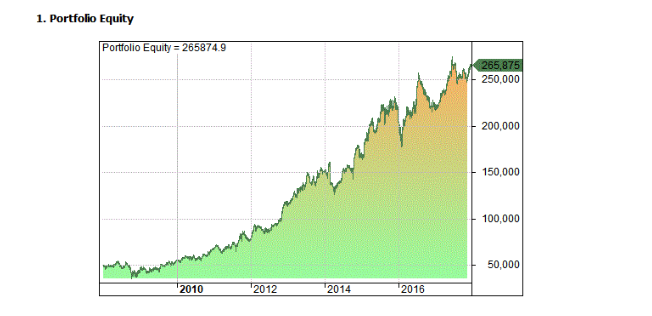

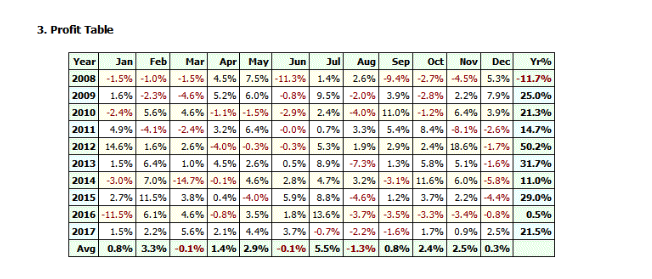

Full Equity Curve 1/2008 – 1/2018 Monthly Table

Monthly Table Key Stats

Key Stats

- Net Profit on $50K: $215,874.89

- CAR: 18.19%

- MDD: -34.42%

- CAR/MDD: 0.53

- RAR: 22.54%

- # Trades: 4240

- Win Rate: 44.91%

Performance Per Symbol (full position size)

Considerations

As you can see from the above, VWAP Pilot shows a decent performance in historical backtesting across a large sample of trades and it has been profitable for 70% of the issues tested.

Of course, it is important to note that these are hypothetical returns and past performance is not always indicative of future returns. (Please see the full disclaimer).

It should also be mentioned that a robust trading strategy can take many months to develop. I have only spent a few days on this and I honestly feel that I have only scratched the surface with this system.

Given the simplicity of this strategy, there may be lots of ways to improve its performance. For example, you could:

- Implement a market timing filter to keep us out of down trending markets

- Use a more sophisticated ranking method

- Investigate different stop losses and profit targets

- Investigate different rules and money management

- Investigate other timeframes & symbols

- Re-optimise parameters according to a walk-forward method

- Use some human discretion in the process

Overall, this is a powerful short-term trading system with room for improvement. It shows strong returns on historical data and can be adapted by the trader for their own use.

Hi JB,

I’ve been daytrading using VWAP and would love to backtesti it in Amibroker. Could you share the code with me? Many thanks!

Omeros

There is a decent code on github, just search on google. thanks