The lottery effect explains our willingness to accept poor odds for a chance to win a huge sum. It’s why millions of us play Lotto or the PowerBall despite huge odds of one in 292,201,338*.

We don’t mind spending a few bucks for the chance to win a gigantic sum, even though the odds are stacked against us.

What Is The Lottery Effect In The Stock Market?

In the stock market, the lottery effect explains why some investors chase volatile stocks and small caps even after they’ve spiked in price.

These stocks appear to have more extreme returns and are therefore more attractive to traders looking to win big.

Here is a good example in RIOT:

Lots of investors became interested in RIOT when it spiked above $20 and then again when it spiked above $30. But they weren’t interested in it before it made those big moves.

The sharp rallies made investors think that this was a stock to keep an eye on. But as a long term investment, buying RIOT after it spiked was a poor choice.

Another example is TLRY:

TLRY attracted a huge amount of attention after it spiked up to almost $300 in 2018 but it ultimately fell back to earth with a bump.

Lottery Stocks Can Become Overpriced

Because of the so called lottery effect, stocks with extreme returns can become overpriced as investors chase them beyond their intrinsic value.

Conversely, stocks with less extreme returns (for example those that haven’t spiked) can end up undervalued and ignored.

That means a strategy of going long less extreme stocks and short more extreme stocks should be a profitable one.

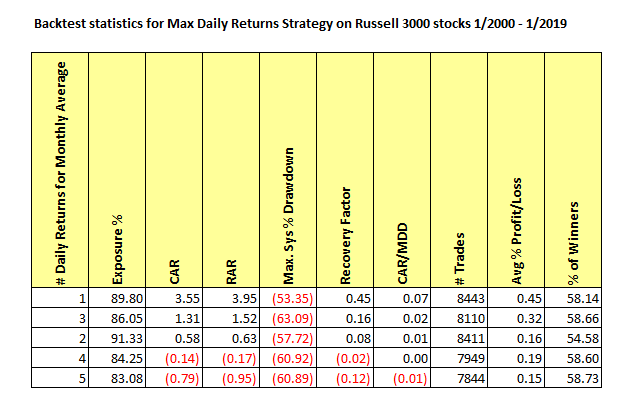

1. Maximum Daily Returns

The website Quantpedia lists one study called the Lottery Effect In Stocks which uses an indicator called MAX to locate stocks with the most/least extreme returns over the previous month.

The strategy is traded on a monthly timeframe and shows an indicated annual return of 13.08% with a Sharpe ratio of 0.32.

(These numbers are taken from the source paper Maxing Out: Stocks as Lotteries and the Cross-Section of Expected Returns.)

Quantpedia describes the implementation of this strategy as follows:

“Stocks are sorted into deciles based on maximum daily returns during the past month. The investor goes long on stocks with the lowest maximum daily returns in the previous month and goes short on stocks with the highest maximum daily returns. Portfolios are value-weighted and rebalanced monthly.”

Backtest Results

In order to backtest this strategy I loaded up my backtest platform Amibroker with historical data from Norgate for all stocks in the Russell 3000.

We then ranked stocks based on maximum daily returns during the past month, where “maximum daily return” (MAX) is defined as the “average of the N highest daily returns (MAX(N)) over the past one month”. We then tested N values from 1 – 5.

In other words, each month we are going to buy the 20 stocks that have the lowest 1-5 daily returns in the previous month and we are going to short the 20 stocks that have the highest 1-5 daily returns in the previous month.

We are also going to avoid stocks with gaps over 30% as these are probably buyouts/mergers.

To avoid illiquid stocks we also discarded any stock under $2 or with a 21-day average turnover less than $250,000. To avoid survivorship-bias we included historical constituents (also referred to as delisted stocks).

As you can see from the table above, the best result came from buying stocks with the lowest 1-day return from the previous month and shorting stocks with the highest 1-day return from the previous month.

We got a CAR of 3.55%, a drawdown of -53% and a CAR/MDD of 0.07.

Overall, you can see that the results deteriorate as you include more days in the calculation of MAX.

The results of this strategy are not good and show that this strategy needs a lot of refinement.

The long side suffers from a fairly short holding length while the short side does not contribute much to the system at all.

2. Skewness

While writing this article I realised that Amibroker already has it’s own built in formula for skewness which we can also use to locate lottery-type stocks.

Skewness (in statistics) refers to a distribution where the curve is distorted (skewed) either to the left or right.

If you think of an ordinary bell curve and then imagine it skewed to the right or to the left you have the right idea.

For our purposes, skewness in a stock indicates how much each daily price point deviates from the mean and the standard deviation of the distribution.

Long Tails In The Stock Market

Skewness is quite prevalent in the stock market because distributions are rarely normal. There is often a long tail caused by extreme daily movements or big winners and losers.

This is essentially how trend following works. Capturing the long tail of stock returns allows you to pay for all of the small losses.

Using the skewness indicator it’s possible to track the level of skewness for any stock on a daily basis based on whatever time period you choose.

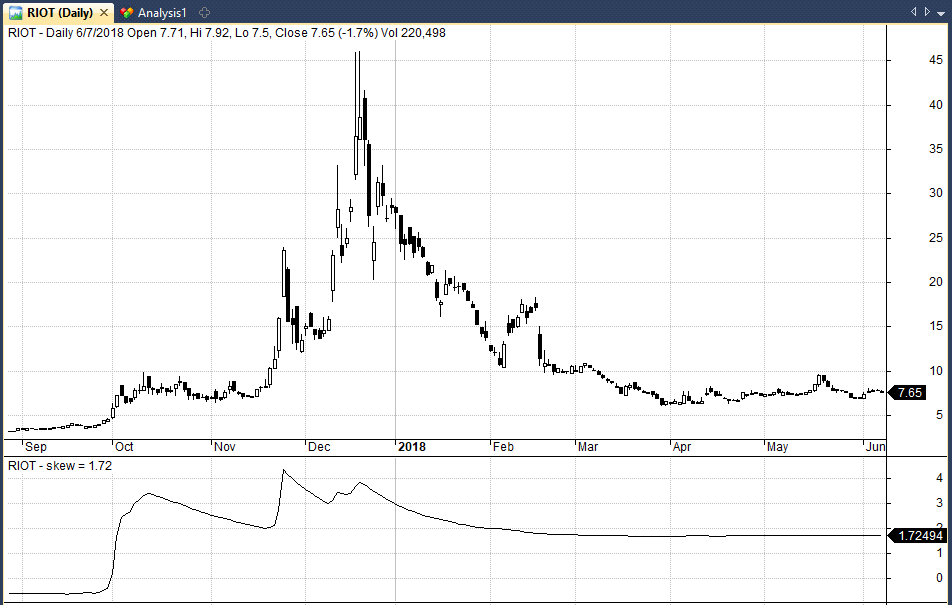

To give you a better idea at the individual stock level, the next chart shows the 252-day skewness indicator plotted against RIOT.

You can see above that skewness jumps over 3 in October 2017 and then over 4 when RIOT spikes above $20.

The more RIOT accelerates to the upside (and the more quickly it does so) the more extreme those results look when compared to the average over the previous 252 bars.

As a result, the skewness indicator shoots higher reflecting the extreme returns.

As you can see in the chart, the skewness scores remains fairly elevated in the proceeding months even as the stock falls back to under $10.

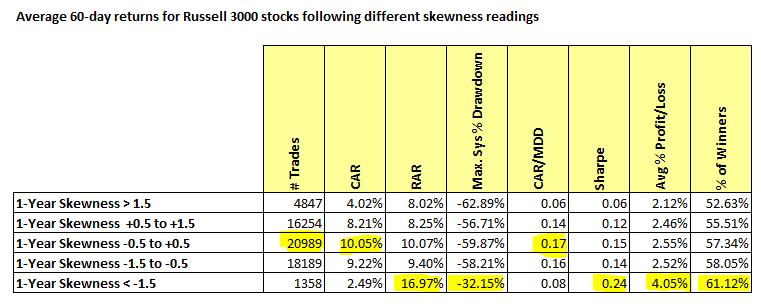

Lottery Stocks Backtest Results

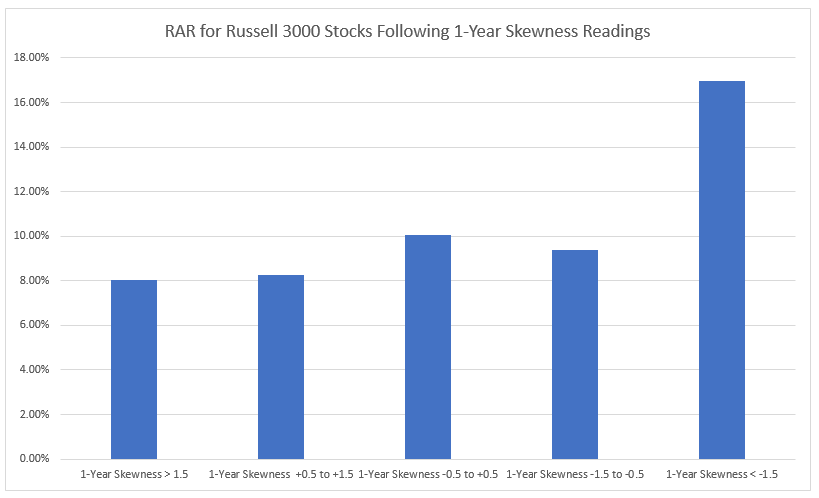

The next table shows backtest statistics for five different levels of skewness for all Russell 3000 stocks between 1/2000 – 1/2018.

Specifically, it shows 60-day returns following skewness readings that range from extreme negative skew to extreme positive skew.

We are using the same backtest settings as previously but with a fixed position size of $1000 per trade:

You can see from the table above that stocks with a high skewness produced poor returns while stocks with a low skewness performed more strongly.

A skewness between -0.5 and +0.5 gave us a compounded annual return of 10.05%, an average profit per trade of 2.55% and a win rate of 57.34%.

Those are decent numbers which could likely be turned into a decent investing strategy.

Meanwhile, stocks with a skew above +1.5 gave us the worst result – a CAR of 4.02% and an average profit of 2.12% per trade.

These results confirm our hypothesis. Lottery-type stocks with extreme skewness produce worse returns than stocks with lower skewness.

The implications of these results seem quite clear.

It’s unwise to invest in stocks with high skewness readings.

Stocks with more normal values of skewness perform much better over medium to long-term horizons.

Stocks with high skewness readings are lottery type stocks that investors chase and usually end up losing on.

There are plenty of other avenues we could go down such as:

- Can skewness be used to improve a trend following or mean reversion strategy?

- Can skewness be used to build a market timing tool?

- Can skewness be used for short selling?

Note: there could be a case for using skewness to locate short-term swing trades or to find stocks suitable for day trading but that is a study for another time.

Conclusions

In this article we looked at the lottery effect in stocks and analysed two methods for locating stocks with extreme returns.

The first method looked at the MAX daily return and was based on a promising academic paper.

However, we were unable to corroborate the results from that paper so perhaps there is a flaw in the methodology or in our analysis.

The second method used the 1-year skewness indicator to locate extreme stocks and we did find some promising results.

Stocks with more extreme skewness clearly showed worse performance over 60-days while less extreme skewness produced much stronger returns.

These results are consistent with our original hypothesis that lottery type stocks make worse investments than less extreme stocks. They also confirm previous analysis that showed lower volatility stocks do better than high volatility stocks.

Overall, the skewness indicator looks like it has merit and could be implemented as one factor in a complete trading strategy. This is a good candidate for further research.

Analysis in this article produced with Amibroker and data from Norgate.