“TSLA is not just pulling customers from BMW and Mercedes but also from Toyota and Honda. Like a magic trick, while everyone is focused on Elon smoking weed, he is quietly smoking the whole automotive industry.”

– Andrew Left

Anyone paying attention to the Tesla stock knows that it’s one of this market cycle’s most interesting stories. What makes it so unique, and almost historic in a sense, is that the company’s detractors are as passionate as it’s supporters.

The company’s CEO, Elon Musk, is often called out for his atypically aggressive behavior for a multibillion dollar CEO, publicly lambasting short sellers of his company.

One of those short sellers is Andrew Left of Citron Research. Or at least he was until October 23, when he reversed his opinion and went long Tesla.

What makes this change of heart so unusual is that Left is still suing Tesla and Musk for violating securities laws, a lawsuit he announced just a month earlier.

Left had been short Tesla since 2013 with his conviction growing, adding to his position multiple times. After five years of pain on the short side, Left flipped his position and got long ahead of Tesla’s Q3 earnings report, with a “worst case scenario” price target of $599.

Almost overnight, Left went from sounding like Jim Chanos to sounding more like Ross Gerber. What gives?

The Bear Thesis (2013)

Left claims to have learned from his mistakes in shorting Tesla and looked deeper into the bull case. Lets compare some of Left’s concerns from his 2013 short report:

- “There is a whole list of potential problems facing Tesla, any one of which holds the potential to trigger a major decline in Tesla stock

- The need to raise capital for CAPEX expenses

- The inability to manufacture and sell profitably without environmental credits (which they have not been able to do yet)

- Competition on the high-end from the world’s foremost prestige brands

- The inability to mass-produce cars affordably in California (Doing business in California has become cost prohibitive, that is why Tesla has the only large scale factory in the state)

- Cannibalization of Model S buyers by the Model X

- Cannibalization of Model S buyers to pre-owned Model S within 2 years

- Failure to penetrate China due to lack of infrastructure to support pure electric competitive domestic manufacturers, and government protectionism

- Failure to establish dealer networks in pushback states

- R&D Expense requirements to create new compelling product (automated cars)”

The Bull Thesis (2018)

When we contrast this with his October 2018 report, most of his concerns from 2013 go unmentioned:

- “Tesla will, finally, after 10 years of unprofitable existence, have the ability to prove that it can be a sustainable, highly cash flow generative entity that is no longer reliant on the capital markets.

- A strong quarter removes the overhang of a necessary capital raise – we suspect that Tesla will be generating more than enough cash to both fund aggressive growth plans and build cash on the balance sheet.

- It transitions Tesla from a “proof of concept” story to a “TAM / how much can this grow” story, attracting a whole new growth-oriented investor base.

- It makes the bear case solely about Valuation and Demand.

- Short interest is at the same (high) level as five years ago though risk is heavily skewed to the upside in the near-term”

While Left doesn’t do a great job of disputing the relevance of some of his 2013 concerns, he does cite some undeniable metrics regarding Tesla’s growth.

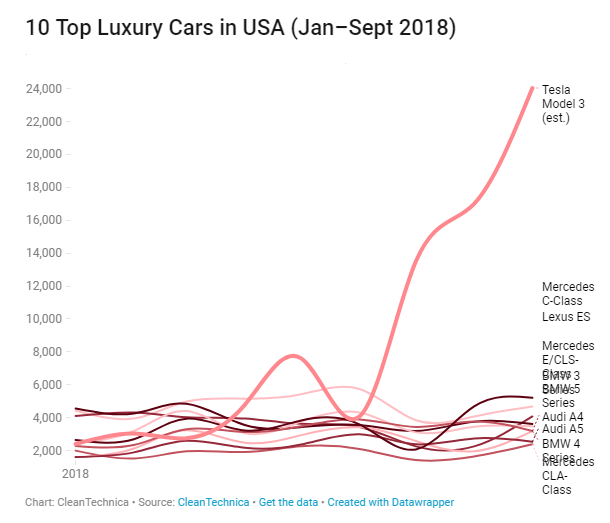

For instance, Tesla is far ahead of the competition when it comes to luxury vehicles, not just electric vehicles, and it’s clear that there’s substantial demand for Tesla cars. The question short sellers seem to be asking is, in the face of this demand, can they turn a net profit?

Further, the way that Tesla is eating luxury sedan market share, you have to ask the question: regardless of Tesla’s profitability, aren’t they always an acquisition target with this growth and demand?

Skepticism From Short Selling Community

Many Tesla short sellers are skeptical of Left’s flip. Some think he’s being disingenuous for a trade, while others think he is simply misinterpreting the data.

Here’s a sampling of tweets from prominent members of $TSLAQ, the Twitter community where Tesla short sellers congregate (a ‘Q’ is added to the ticker symbols of bankrupt companies).

https://twitter.com/ElonBachman/status/1054747577097154560

https://twitter.com/NetflixAndLamp/status/1054829054099181573

https://twitter.com/Paul_M_Huettner/status/1054753386430631936

Conclusion

The fact remains that, as far as we know, Left’s class action lawsuit against Musk and Tesla is still active. Common sense tells us that if Left is a long-term Tesla bull, he would not want to harm the company with a public lawsuit.

Regardless of his intentions, Left is killing it.

Here’s how he’s done so far:

Assuming he bought shares a day ahead of his report, he probably bought between $261 and $252 (Oct 23’s high and low), which would be about a 30% gain, assuming he is still holding the position.

That’s a great return in just a couple of weeks. But who knows, after that sort of gain maybe he’s ready to flip once more.

Disclosure: The author currently holds a short position in Tesla stock.