We collected 70 short-selling reports (since 2015) by two well-known short-sellers, Hindenburg Research and Muddy Waters Research. As our analysis shows, roughly 67 percent of the short recommendations actually traded lower a year later, and the short bets can make you money.

What Is Short Selling?

Going short a stock is selling it now, without really owning it, and buying it back later. When would you do this? Whenever you have a strong believe that a stock’s price will be lower in the future. If so, you can buy it back cheaper and pocket the difference.

Usually shorting is done using a margin trading account. To sell a stock that you do not own, your broker would find the stock to borrow.

You could also short a stock using options (buying a put option). This is called a synthetic short.

Short selling is risky as theoretically you can lose more than the money in your brokerage account. A stock can go up 100, 200, 300, or more percent, and the price increase is the short-seller’s loss.

That’s why if you make a short bet, you need to have a lot of conviction and sound risk management.

Let’s look at some famous examples.

Herbalife Short

If you were following the markets back in 2012/13 you will probably remember the cover story of Bill Ackman shorting Herbalife. Ackman (Pershing Square Capital Management) held a public presentation claiming that Herbalife was a pyramid scheme with a highly doubtful future. He opened a short position that at it’s peak cost him around $1 billion USD.

In early 2013, activist investor Carl Icahn (Icahn Enterprises) took the opposite side by investing in the stock and starting a personal feud with Ackman, all on live CNBC.

How did it go?

While Ackman’s bet looked promising at first (the stock lost -30% in the days after the presentation), the direction switched in spring 2013, with the price soaring to over $40. That’s double what it was worth in December 2012.

Carl Icahn tried orchestrating a short-squeeze, as he tried to drive up the price so that short investors would have to cover, thereby pushing it up even further.

Allegedly, Ackman lost close to all of his stake while Icahn made close to one billion on the trade. There was an interesting documentary on the case called Betting On Zero, mostly showing Bill Ackman’s perspective.

Gamestop Short

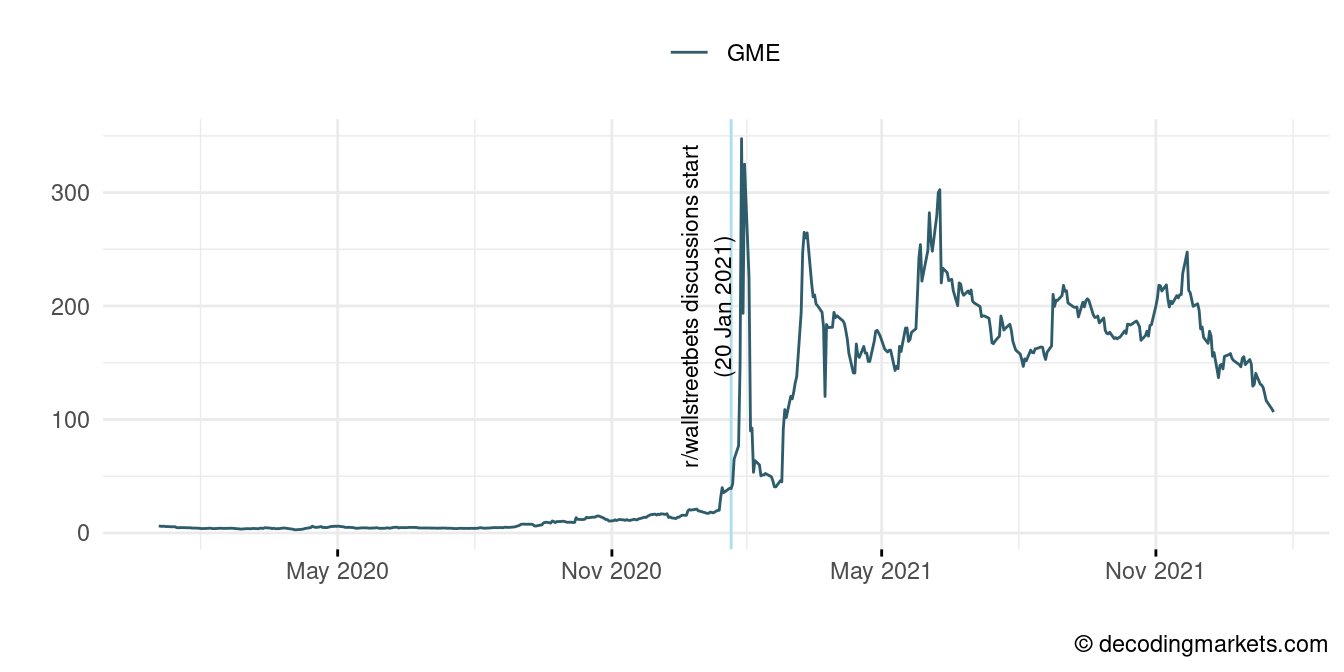

This leads us to the second and more recent example: Gamestop (GME). We’ve all heard the story by now. Hedge fund short-sellers, namely Citron Research and Melvin Capital, went short while some maniac Reddit traders went long. How did this turn out?

While the short-sellers surely had a point (the business model of reselling physical game disks was reaching it’s expiration date), their bet did not go as expected. A massive short-squeeze changed everything and GME peaked at $380 on 27 January 2021, which is a 2,200 percent increase from the $17 it was trading at the start of 2021.

It’s not known how much the short-sellers lost but you can assume that the losses were substantial.

In other words, short sellers need to be sure of their bets as things can go bad very quickly. Even with the most attentive due diligence, you can’t be right all the time, as can be seen from these two examples.

Hindenburg And Muddy Waters

Many funds take short positions occasionally without the public knowing about. At least in the US there is no legal obligation to disclose any short stock positions, contrary to long positions which are published in 13F filings. (You can check out our strategy backtests using institutional trading data here and here).

There are, however, two institutional short-seller that frequently release what’s called short-selling reports: Hindenburg Research and Muddy Waters Research.

As a side note, there was also Citron Research, but the fund’s manager Andrew Left stopped putting out short-reports after the Gamestop incident.

Hindenburg Research received public attention after their claims of irregularities in Nikola (NKLA) in September 2020. One accusation was that in a promotional video, their e-truck prototype was simply rolling down a slope. The stock tanked over the following weeks. Hindenburg has been around since 2017.

Muddy Waters Research is a further outlet of short-reports that has been around since 2010. The company by Carson Block uncovered misleading accounting practices and inflated sales figures in US listed Chinese stocks. There’s a documentary called The China Hustle worth watching (depending on your country you can find it on Netflix).

Our Analysis On Short Sellers

We have collected all short-selling recommendations from both Hindenburg and Muddy Waters. We double checked using the Web Archive if any content had been removed (none had!). We then collected price data from our usual data source (Norgate Data), because it’s crucial to also get your hands on delisted stocks. In case of the few non-USD stocks, the prices were converted to USD.

One more thing to note: We will show the immediate price impact from the close price of the report publish date to the next day’s close (“1-day return”), and we will show the 3/6/12-months returns for which we exclude the very first day. The idea is that we do not know at what time Hindenburg or Muddy Waters released the reports (before or after trading hours). Also traders might be late, so giving a day in between makes the analysis more realistic.

So how did the short recommendations perform?

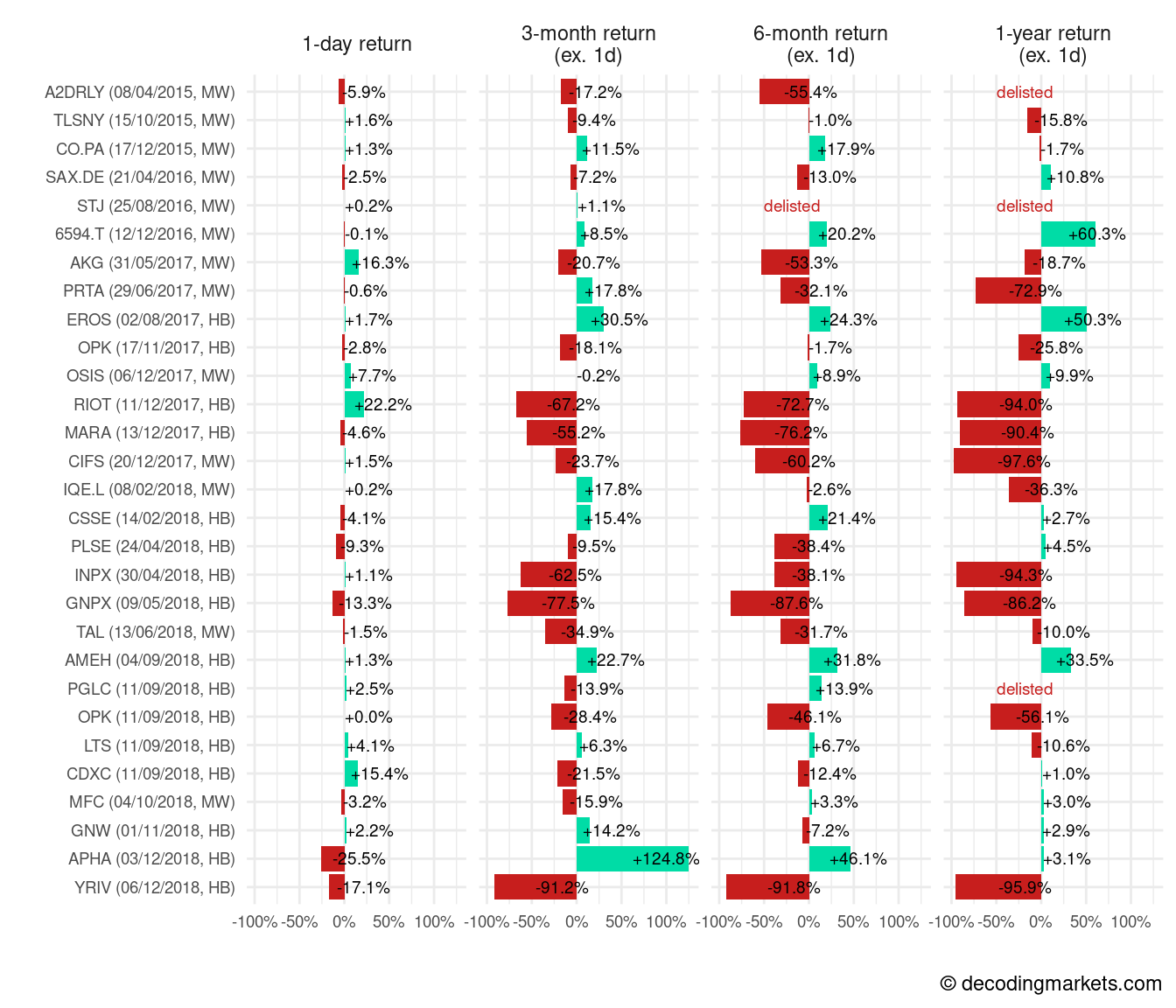

Looking at the short picks from between 2015 and 2018 (Hindenburg since 2017, and neglecting the Muddy Waters picks prior to 2015 due to partially unavailable historical stock data), we see mostly red. In other words, many of the stocks went down. Exactly what we want to see.

The most successful shorts by Muddy Waters (MW) were Noble Group Ltd (A2DRLY, delisted), Prothena (PRTA, -72.9% a year later), and China Internet Nationwide Financial Services (CIFS, -97.6%, renamed Hudson Capital, ticker HUDS).

By Hindenburg (HB) we had Riot Blockchain (RIOT, -94%), Marathon Patent Group (today Marathon Digital Holdings, MARA, -90.4%), Inpixon (INPX, -94.3%), Genprex (GNPX, -86.2%), and Yangtze River Port & Logistics (YRIV, -95.9).

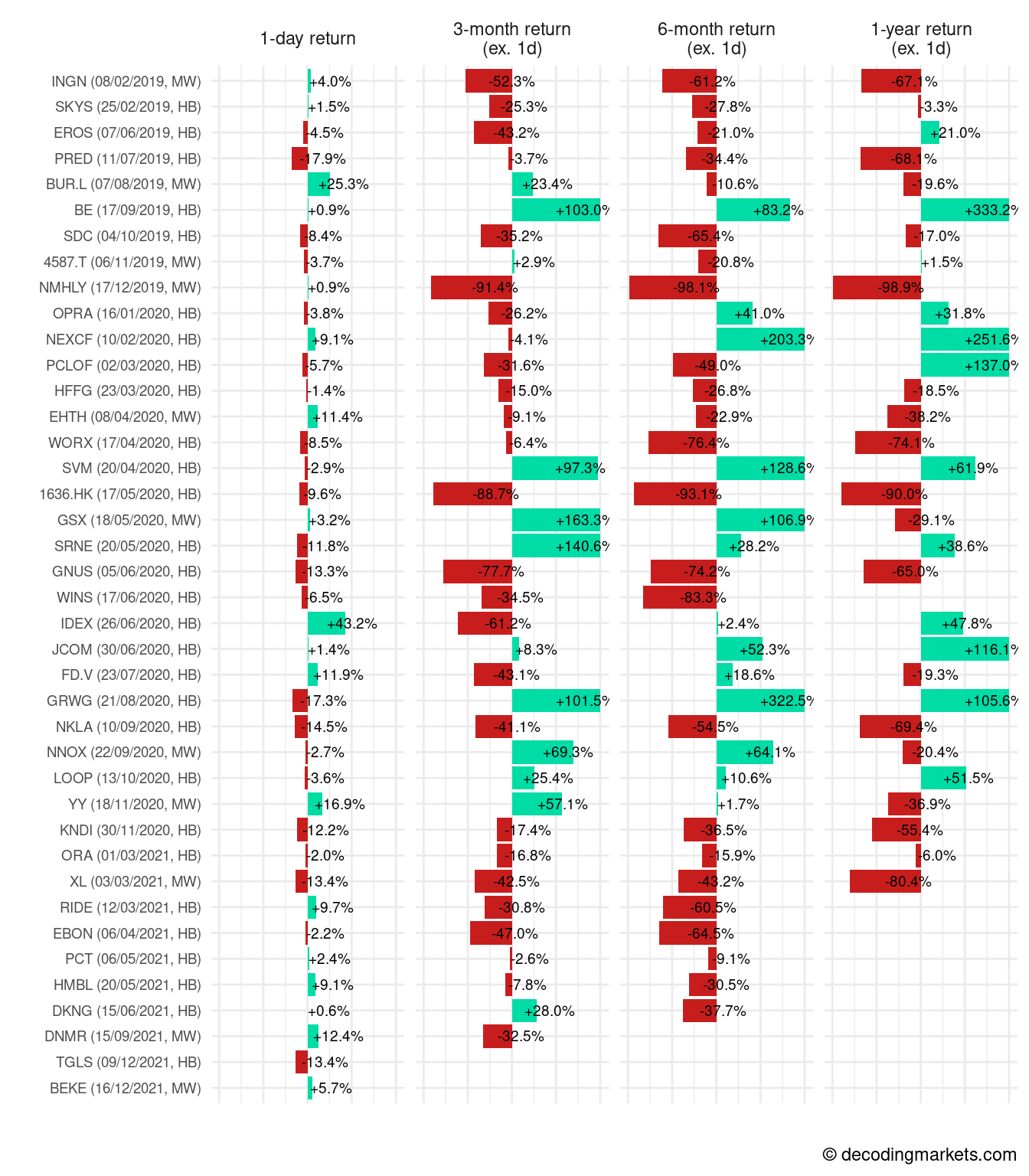

Since 2019 the picture looks more green overall with a few stocks up more than 100%. But let’s discuss the correct predictions first.

From Muddy Waters we find Inogen (INGE, -67.1% after a year), NMC Health plc (NMHLY, -98.9%), and XL Fleet Corp. (XL, -80.4%). There are no instances of stocks up after 12 months, even though we had GSX Techedu (now CSX Corporation, GSX up more than 160% a few months after the short had been reported (it still dipped lower later though).

Hindenburg’s picks were more mixed, with a few picks down substantially, namely Predictive Technology (PRED, -68.1%), SCWorx (WORX, -74.1%), China Metal Resources Utilization (1636.HK, -90%), Genius Brands (GNUS, -65%), and of course Nikola (NKLA, -69.4%).

On the opposite side, there are some picks that contrary to Hindenburg’s analysis did not erode. We find Bloom Energy (BE, +333.2%), NexTech AR (NEXCF, +251.6%), PharmaCielo (PCLOF), J2 Global (JCOM, turned into a new company trading as CCSI today, +116.1%), or GrowGeneration (GRWG, +105.6%).

Here are the overall stats (all excluding the the first day from the report release):

- median 3-month return: -13.9% (mean -5.5%)

- median 12-month return: -15.8% (mean -5.5%)

- percentage down or delisted after 12 months: 67%

Short Report Strategy

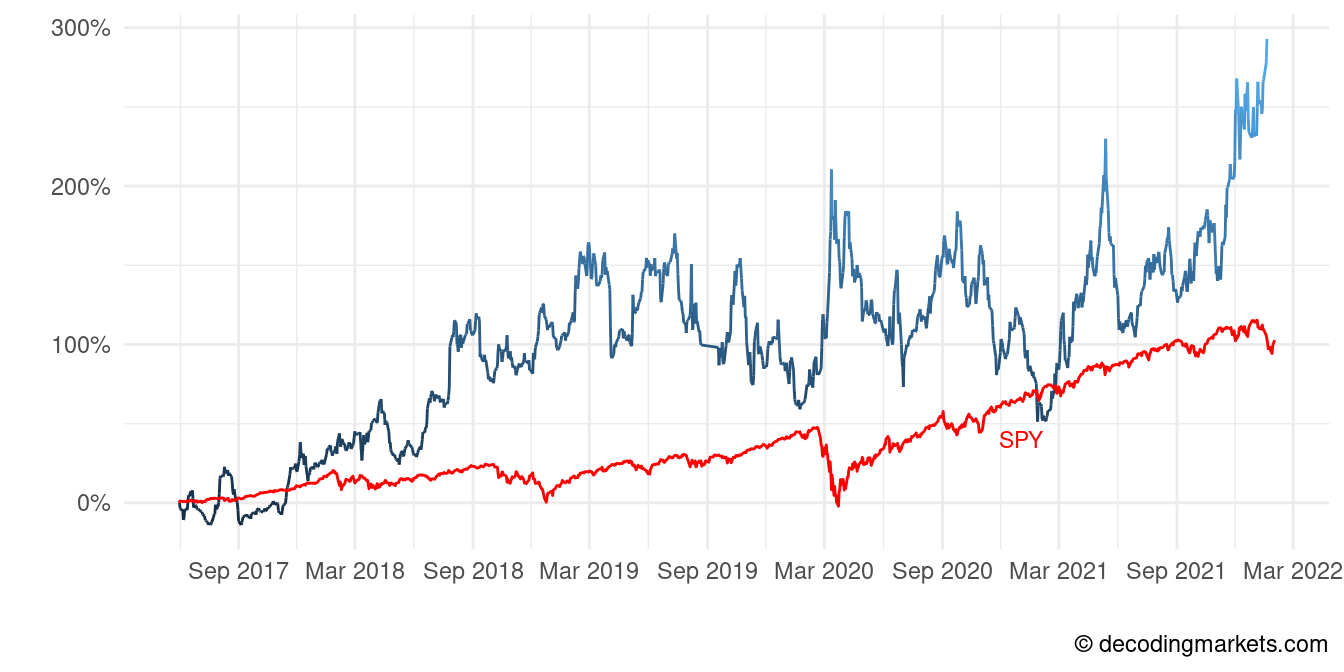

How would a strategy that shorted all short recommendations by both Hindenburg and Muddy Waters have done?

Very volatile, have a look below:

Our backtest delivered an annualized return of 27.7% at a standard deviation of 45.5% (Sharpe ratio 0.61) since 2017. We assumed a maximum holding period of six months (125 trading days) and a stop-loss at -35%. Without the stop-loss, the few wrong predictions by Hindenburg since 2019 would have hammered the performance down.

Note: we did not take into account any cost of shorting or borrowing fees which would drag the returns down further. In the case of some small cap stocks with high short interest, the borrowing costs can be substantial and difficult to implement.

Final Thoughts

Investigation of stock markets, including identifying poor business models and fraud, is important work. Especially in today’s financial world where investors are bombarded with hyped up powerpoints and exaggerated forecasts.

Even with passive investment vehicles like ETFs, investors are often dazzled by environmental and social claims, without having enough knowledge of the businesses they are investing in.

Short sellers provide a natural balance to this froth. They are wrong occasionally, and many stocks are hard to short. But it’s still useful to read their reports. Our analysis shows that reports from Hindenburg and Muddy Waters provide real value to long and short investors.

Notes: Data from Norgate. Simulations produced in R, Excel and Amibroker.