Visa Inc. ($V) is a multinational financial services company that facilitates the transfer of funds around the world via Visa-branded credit cards and debit cards. If you didn’t already know that you must be living on another planet because Visa is everywhere. Here are 10 reasons why you might want to buy the stock today.

10 Reasons To Buy Visa Shares

#1. Great looking chart

The first reason to buy Visa relates to the monthly chart which you will see posted twice below. It’s quite simply one of the best looking charts around with multiple consecutive higher closes and higher lows. A very strong trend. You will not find a much better chart in all your years of investing.

#2. Almost a fourth consecutive lower month

Sticking with the monthly chart, you can see that the stock is currently in line to post it’s fourth consecutive lower monthly close.

Visa has not fallen more than three months in a row since 2008 (during the financial crisis the stock fell five consecutive months before trending higher). In other words, Visa rarely falls for this long and the odds suggest that the bottom may be around the corner.

#3. Two hammer patterns

Also, the previous two months of this year (January and February) have been hammer candlestick patterns with very long lower shadows. This price action suggests sellers have been unable to keep the stock down for long before it’s been bought back up by investors. The stock does not seem to like it much below the $70 level as buyers always seem to step in. We also saw a much bigger hammer in August last year before going higher.

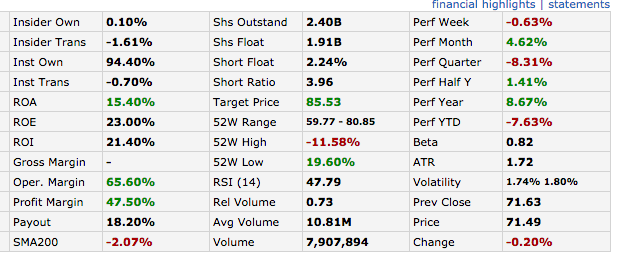

#4. High Return on Equity (ROE)

Visa is currently the 21st largest company in America with a market capitalisation of $171.68 billion at the time of writing. Even so, the company boasts an enviable Return on Equity ROE of 23%. Only three companies in the top 20 have a higher ROE and they are Apple, Verizon and Coca-Cola. And by the way, Warren Buffett says that ROE is one of the most important factors when buying a stock.

#5. Excellent profit margins

As well as having a high ROE and impressive EPS growth (30.6% over the past five years) Visa also has an operating margin of 65.60% and profit margin of 47.50% (see image above).

There is no doubt that the credit card business is one of the most lucrative business models you could dream up. Visa has been at the forefront of it for many years.

#6. Visa is everywhere

As I mentioned at the beginning of this article, Visa is a truly global company and you can find Visa-branded credit cards and services all over the globe. There is hardly a place on earth now where you can’t use a Visa credit card to pay for something.

In fact, Visa and Mastercard ($MA) operate a real and lasting duopoly which gives both stocks a huge competitive advantage in the field. There is no company that can compete with these two giants which makes both stocks great investment choices. For me, the competitive advantage, solid business model and huge brand are the biggest reasons why this stock is a buy.

#7. Cash has had its day

When was the last time you took out a wad of cash from the bank machine and used it to pay for… well anything?

OK, maybe you do still use cash now and again but there’s no doubt that we are rapidly moving to a paperless economy and that means demand for credit cards and contact-less payment services will continue to be in high demand. Even services such as Apple Pay will no doubt need to link up with operators like Visa and Mastercard.

#8. Visa is investing in new technology

And don’t forget that Visa already has its finger on the pulse when it comes to new technology and the new paperless economy. Visa employees are currently working hard on new innovations that will work in mobile phones, cars and other devices. You can also see Moody’s recent study into the impact of digital payments here.

#9. Visa is in Emerging Markets

Although Visa is just about everywhere there are still places where the company can still grow and the company is expanding all over the globe, particularly in China (where it recently forged a deal with China Union Pay) and Emerging Markets. Yes, Mastercard probably has a stronger foothold in China than Visa right now but there should easily be enough for both companies to prosper.

#10. Warren Buffett owns Visa

Lastly, investment legend Warren Buffett owns Visa and who are we to argue with an investing genius? Buffett’s investment company Berkshire Hathaway has owned Visa for many years now and has only increased his holding as time has gone on. It seems like one of those stocks that he never wants to sell.

Rounding-up

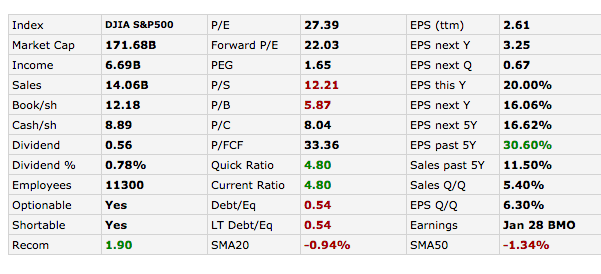

With a price-to-earning ratio of around 27, you wouldn’t class Visa, at this point in time, as being remarkably cheap.

But the problem is that quality businesses like Visa rarely trade at low multiples because their finances and business models are so strong. The only time you will be able to get in a stock like Visa at a really low multiple is likely to be during a severe market crash and that’s an unlikely prospect.

Looking at the chart, the stock has fallen three months in a row (a rare occurrence) so this seems like a good time to take a small position or add to an existing position. This is the kind of stock you want to keep in your portfolio for the long haul.